The overnight policy rate (OPR) is currently at a record low of 1.75%. In May last year, Bank Negara Malaysia cut the OPR to 3% — the first revision in more than a year at the time. Before that, the OPR had been kept at 3.25% since January 2018.

This article first appeared in theedgemarkets.com. View source here.

The central bank subsequently announced more OPR reductions, and with the latest 25-basis-point cut on July 7, the rate has been reduced by a total of 125bps so far this year.

Hong Leong Investment Bank Research (HLIB Research) does not discount another 25bps cut to 1.50% as early as Bank Negara’s next monetary policy committee meeting in September, as economic activity is expected to remain weak and inflation prospects modest.

“Despite expectations of gradual improvement in Malaysia’s growth prospects, the pace and strength of the recovery remain subject to downside risks emanating from domestic and external factors,” it says in a report.

HLIB Research adds that policy measures implemented domestically to mitigate the negative impact of Covid-19 will lapse in October, putting downside risks on the economy, while sluggish and uncertain growth could lead to further job losses and deter investment.

A standstill

Many have said that now is the best time to buy a property because of the low-interest rate and willingness of developers and property owners to sell their properties at lower prices to maintain cash flow.

Photo by Low Yen Yeing/EDGEPROP.my

Nevertheless, the Movement Control Order (MCO) and the subsequent Conditional MCO that was imposed to contain the Covid-19 pandemic have hit the economy significantly. Businesses are closing down and many employers are cutting their employees’ salaries to keep their companies afloat.

How badly has the property market been affected during the MCO period?

Activity in terms of new launches and transactions is expected to be slow in the residential market in 2020 amid the economic headwinds and job insecurity. Developers are focusing on clearing their inventories instead of new launches.

Nawawi Tie Leung managing director Eddy Wong tells City & Country that the larger concern on everyone’s mind is the Covid-19 pandemic, its impact on the global economy and the impending recession with its attendant problems such as distressed companies and job losses, which will affect homebuyers’ sentiment.

“This is against the backdrop of the property market being in an oversupply situation even before the pandemic,” he says.

There are fears that there will be another round of MCO if the Covid-19 situation cannot be controlled. If that happens, it will further dampen economic and job recovery. The chain of effects may result in more fire sales.

Property consultants generally do not expect to see fire sales for now — at least not until after September — due to the six-month loan moratorium announced by Bank Negara that provides financial relief to many people.

While the number of fire sales in the property market is not high at the moment, CBRE|WTW managing director Foo Gee Jen observes that there may be isolated cases of more desperate sellers mainly because they are experiencing cash flow problem.

“Lately, sellers have been more receptive to offers by prospective buyers. Similarly, in the capital market, the Securities Commission Malaysia commented that there has been no escalation in redemptions of unit trusts so far. This could be interpreted as the market being in contemplation and in a ‘wait and see’ mode,” he says.

Photo by Low Yen Yeing/EDGEPROP.my

“The prudent lending by banks in the past could have helped to ensure property owners, by and large, possess holding power. In fact, guidelines by Bank Negara advocate more flexibility and leniency among banks in loan restructuring and refinancing. This bodes well for keeping default risk down, and if the situation turns bad, we expect the market will be resilient enough not to crash but experience a soft landing.”

Wong notes that the fire sales will most probably come from property owners who may have overstretched themselves by buying several properties during the good times and are now finding it difficult to sell or rent out the properties. There are also those who have lost their jobs and can no longer afford to service the loans.

“The OPR cut will assist some of these owners, bringing some respite to those affected by job or salary cuts. This is on the assumption that the housing loan interest rate is floating, which means it moves in line with the prevailing interest rate and is not a fixed rate housing loan,” he says.

Lower OPR and buying properties

With the lower OPR, property consultants reckon that now is a good time to buy a property, as a low interest rate means lower barriers to financing and owning a property. They believe the residential sector will remain a buyer’s market moving forward, with further discounts, rebates and promotions from developers.

It is important for buyers to be selective and look out for properties with good location, connectivity and amenities. As for investors, they need to make sure that the property can be rented out easily, or they have sufficient cash flow to cover the mortgage.

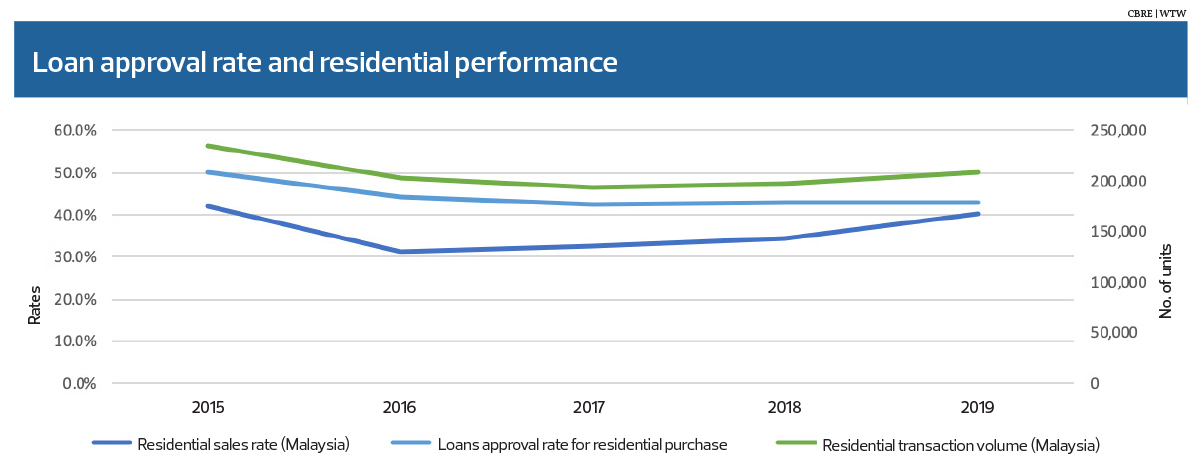

Foo says in the past five years, sales in the primary market and overall transaction volumes in the residential market generally moved in tandem with the loan approval rate for residential purchases (see chart).

“In 2019, these three indicators shared an upward trend. In the present scenario, low interest rates and the expected further cut in OPR would incentivise residential purchases for those who are financially sound,” he explains.

If and when Bank Negara adjusts the OPR upwards, it would also mean that the economy is recovering, and the higher inflation rate would then translate into higher property prices. Wong says the adjustment of interest rates depends on several factors, such as the recovery of the economy, the outlook for inflation, business confidence and the ringgit exchange rate.

“Given that the impact of the pandemic is global, we think the recovery may take a little while longer to gather momentum … but it is definitely a good time to buy as developers will be offering discounts and rebates to persuade homebuyers to buy in the current market,” Wong says.

“It is no doubt a buyer’s market and those who are considering buying a property should capitalise on the current depressed market and seize the opportunity to secure a good buy. This is probably a once-in-a-lifetime opportunity that should not be missed.”

Foo notes that the fundamental cause and implications of the Covid-19 crisis are different from the Asian and global financial crises, and that past trends may not be relevant in this unprecedented event.

“Monetary adjustments are the prerogative of Bank Negara, bearing in mind the central bank also manages inflation and currency. The general expectation is for more cuts in the OPR in the near future before we could see an upturn in the economy,” he says.

“[A higher effective lending rate] will increase the mortgage repayment for non-fixed rate loans, while the cost of borrowing for new applicants will increase. It is one of the factors driving up house prices over time.”

For residential property loans, the effective lending rate is calculated by adding the base rate (BR) and the spread rate. As the BR is based on the banks’ benchmark cost of funds and the statutory reserve requirement, banks can revise the BR at any time, even when there is no change to the OPR. Meanwhile, the spread rate is determined by the borrower’s credit risk and liquidity as well as the banks’ operating cost and profit margin.

Foo has calculated the differences in terms of monthly repayment, total loan payable, total interest payable and ratio of interest to principal depending on the effective lending rate (see table). The illustration is based on a property valued at RM500,000, with a total amount financed of RM450,000 (10% or RM50,000 for down payment) for 35 years.

At an effective lending rate at 3.75%, the monthly repayment of the home loan is RM1,925.57. At the end of the loan tenure, the buyer would have paid RM808,741 in total, with 44% being interest charges.

Meanwhile, if the loan were at an effective lending rate of 3.25%, the monthly repayment would be RM1,795.22. After 35 years, the total loan paid would be RM753,992, of which 40% is for interest payment.

“In every crisis, there will be opportunities to pick up good assets. Property is a hedge against inflation and Malaysian properties have lived up to that expectation in the past. The principle of real estate such as location and quality will continue to be the main determinants of property value,” Foo points out.

“For homeowners, do your research and buy within your affordability, and for investors, stick to the basics of yields and returns. As we adapt to the new norm of social distancing, it is time to rethink our idea of ‘home’ with regard to safety and privacy.”